Reports

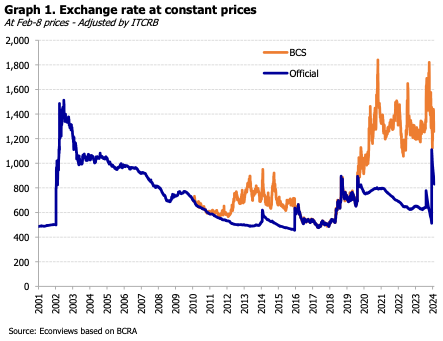

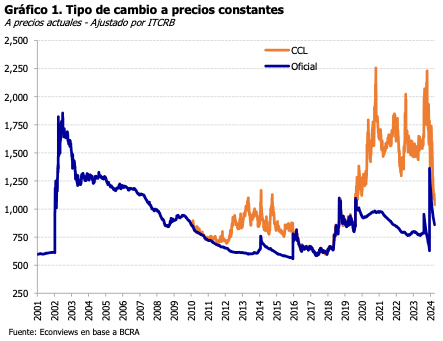

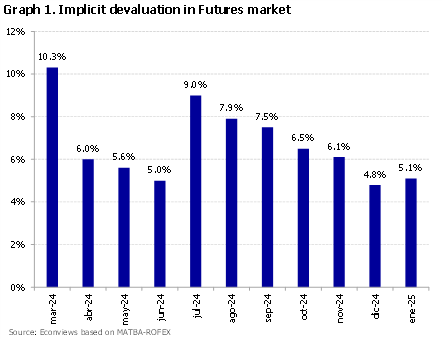

It seems that the government has no plans to remove FX restrictions in the short term. It also seems less likely that there will be a shock stabilization plan such as the Austral or Convertibility plan. We changed the exchange rate unification that we had projected in July to December. For the next few months, we think that the crawling peg will continue at 2% until the harvest ends and then there will be a slight acceleration. By the end of the year, we see a dollar of 1,600 pesos with the unified market. The magnitude of the FX spread will depend on whether the government relaxes the restrictions on the Blue-Chip Swap or not. In the first case it can rise more than in the second.

- weekly

Support for Reforms in the Lower House, More Rate Cuts and Less Subsidy Cuts

The government is approaching critical times as Congress is starting to debate the “Ley de Bases”. The bill includes a fiscal package as well as some structural reforms that should help to improve productivity and increase investment and growth. This is a tone down version from the law that was sent to Congress in February and then withdrawn because the government considered that Congress was softening it too much.

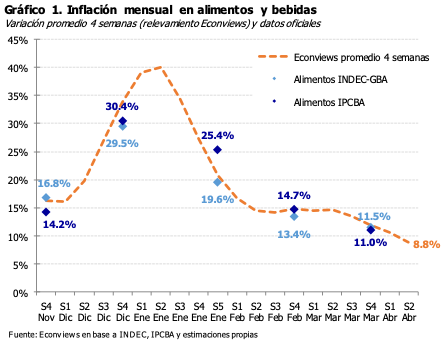

Los datos de alta frecuencia que medimos en cadenas de supermercados del Gran Buenos Aires (alimentos y productos de cuidado personal) nos mostraron una deflación por primera vez desde que hacemos este ejercicio. Hay muchos peros porque nuestra canasta no es idéntica a la del INDEC y la muestra de comercios es más chica, pero aún así en los últimos meses los alimentos que medimos tuvieron trayectoria bastante similar a la de los subíndices de alimentos del índice de la Ciudad de Buenos Aires y la del INDEC para el Gran Buenos Aires.

One of the key points of the economic program is to achieve fiscal balance this year. We think the government will try, but it will probably not make it. We estimate the year will end with a balanced primary result and a fiscal deficit of 2% of GDP. In any case, a result like this would be well received by the market.

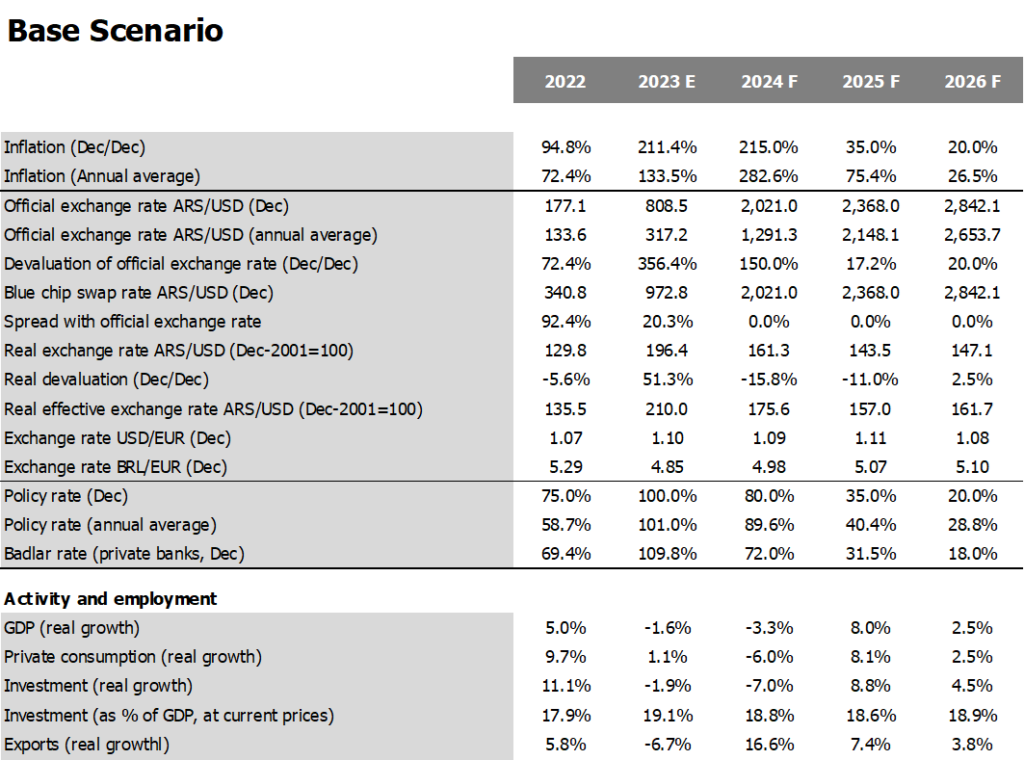

Monthly inflation figures will remain declining, but high due to the increase in regulated prices. The emphasis will be on reducing subsidies through the adjustment of utility bills and transport rates. We expect double-digit inflation rates until April. Once the relative price adjustment ends, we believe that monthly inflation will remain at around 6%. To get below that number, a stabilization plan will be needed. It could be similar to the Austral plan, the Israeli plan, the Real plan, convertibility, or even the dollarization. We expect it to be launched in early 2025.

1) How would the economy look at the end of 2024 to be considered a success? A successful adjustment would mean most of the following features. Firstly, the inflation rate has to be comfortably in one digit. We think that unless there is a conventional stabilization plan (i.e. a regime change) inflation will hover around 6-7%. That fits the criteria of one digit, but it is probably higher than what the government is hoping for.

The first 100 days of Milei’s government have already passed. An experiment for the Argentine political system. As has already been demonstrated in this short time, politics is precisely the weakest link in Milei’s management. The main figures in the government have no experience in the public sector and the establishment also has to get used to a new form of communication and politics that Milei imposes.

The opening of ordinary sessions of Congress left a lot of content to analyze. There were insults towards politicians. The middle class in general supported the speech and there was a conciliatory ending. Relief for the provinces and the May Pact. Beyond the president’s particular style, in the end we all know that seeking consensus is a healthy starting point to reduce the volatility of the Argentine economy, perhaps the most obvious symptom of structural imbalances.

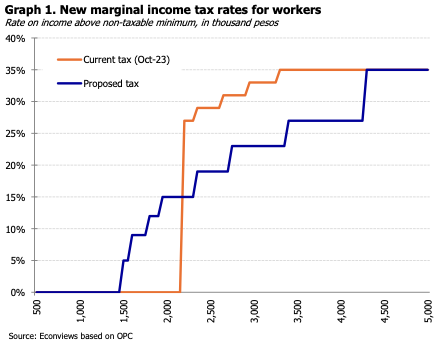

One of the main axes of the economic program is to achieve fiscal balance this year. We believe that the government will try, but probably will not be able to get there. We already saw complications in Congress when attempts were made to raise taxes. Now the government is going to try to make tax reforms again within the “May Pact.” We think that the year will end with primary balance and a fiscal deficit of 2% of GDP. A result like this would be more than positive.

The national government is embarked on the mission of improving national accounts by 5 points of GDP. We are not so optimistic, but we believe that it is very likely that at least a primary balance will be achieved, which would be very commendable to achieve in a recessive year. Furthermore, we believe that if primary balance is achieved, the country’s risk could fall to half of what it is today and drop to around 800 points by early 2025.

Javier Milei has had a good beginning on the economic front. Investors like what they see, the IMF supports his policies, and the US has been sending top government officials to visit Buenos Aires, a gesture that is welcome by the government. Despite the tough policy measures that have been implemented Milei´s popular support remains high with a positive image of around 50%.

This week Gita Gopinath, number 2 at the IMF, visited Buenos Aires. She came with part of her team and met with President Milei and several figures from the private sector. She was complimentary of the program and outlined some challenges the economic team will face in the coming weeks or months. We took advantage of her visit and we also reviewed these 78 days of management.

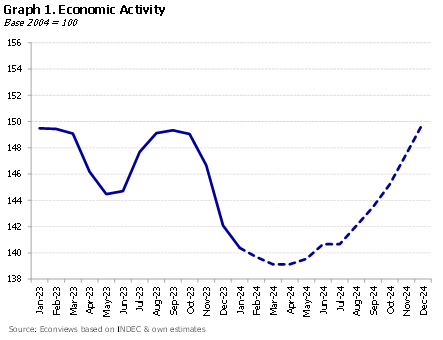

Argentina is going through the worst moment of the recession. This was to be expected given the necessary rearrangement of relative prices that, although underway, has not yet ended. The president warned about it when he took office, talking about “stagflation.” The vast majority of consultants also estimated a drop in activity in the first months of the year. It’s one thing to say it and another to live it. The frustration of many families with loss of purchasing power, of merchants and industrialists who do not sell is more than understandable. It is at the same time a political threat to the government since public opinion less than 3 months ago told Milei to move forward, but perhaps not everyone was aware of the inevitability of a severe adjustment.